Couples, income split. One has the relevant shares in their name and have an income below the tax threshold.

Quote Jim "It doesn't affect investors with a portfolio providing annual dividends higher than $37,000 who are in a higher tax bracket than the company tax."

They still have the first bit tax free, the next at 19c so the overall rate is lower.

Income of $40 k is not all at 30c, but 18K zero and the next 19K 19c then the last 3K at 32.5c, which would give a tax rate of about 9.5c.

Abbott/Liberal Govt Watch

Re: Abbott/Liberal Govt Watch

![]() by DOC » Sat Mar 02, 2019 12:50 pm

by DOC » Sat Mar 02, 2019 12:50 pm

Re: Abbott/Liberal Govt Watch

![]() by DOC » Sat Mar 02, 2019 12:54 pm

by DOC » Sat Mar 02, 2019 12:54 pm

With all thats been said/posted, it is never a good system to treat people differently as it will cause issues for some that others don't get.

Re: Abbott/Liberal Govt Watch

![]() by Jimmy_041 » Sat Mar 02, 2019 3:48 pm

by Jimmy_041 » Sat Mar 02, 2019 3:48 pm

DOC wrote:Couples, income split. One has the relevant shares in their name and have an income below the tax threshold.

Quote Jim "It doesn't affect investors with a portfolio providing annual dividends higher than $37,000 who are in a higher tax bracket than the company tax."

They still have the first bit tax free, the next at 19c so the overall rate is lower.

Income of $40 k is not all at 30c, but 18K zero and the next 19K 19c then the last 3K at 32.5c, which would give a tax rate of about 9.5c.

Correct, but you can only do that if you invested through a trust. We didn't have one in the 90's so most of our shares are in my wife's name to minimise the tax, but, the main point is: as you earn more; you pay tax and therefore you reap the benefit of the excess credits.

So; it actually targets the lower and middle class, and in all probably, never the wealthy.

This is what Robert Gottliebsen is saying.

I might add; it applied to pensioners as well until they did a massive backflip and added the Pensioner Guarantee

https://www.theguardian.com/australia-news/2018/mar/27/labor-offers-pensioner-guarantee-as-tax-policy-divides-voters-guardian-essential-poll

dedja: Dunno, I’m just an idiot.

Re: Abbott/Liberal Govt Watch

![]() by Q. » Sat Mar 02, 2019 10:04 pm

by Q. » Sat Mar 02, 2019 10:04 pm

Jimmy_041 wrote:DOC wrote:Yes

Quoting Traders example above

The person in the 0% bracket gets a full refund.

Someone in the 19c bracket gets 11c back.

Someone in the 45c bracket pays the additional 15c.

And from CommSEC

Case study: James receives a tax refund

James owns shares in a company. The company pays him a fully franked dividend of $700. His dividend statement says there is a franking credit of $300. This represents the tax the company has already paid. This means the dividend, before company tax was deducted, would have been $1,000 ($700 + $300).

Come tax time, James must declare $1,000 (the $700 dividend plus the $300 franking credit) in his taxable income. If his marginal tax rate was 15%, he would have paid $150 tax on the dividend. Because the company has already paid $300 in tax, James will receive a refund of the difference, which is $150.

If James was in a higher tax bracket he may not have been entitled to a refund of any of the franking credit, he may even have to pay additional tax. However, if he is a low income earner, it is possible to be refunded the full amount of the franking credit.

So, this change to the tax treatment of the excess credits will 100% affect those investors with shares providing total dividends up to $18,200, and partly up to $37,000 depending on the franking rate. It doesn't affect investors with a portfolio providing annual dividends higher than $37,000 who are in a higher tax bracket than the company tax.

The average dividend yield is 2.5% so to reach $18,200 in dividends, the average portfolio would have to be $728,000. Remembering this is outside super, that would probably affect all poor, struggling, emerging and the majority of middle class families?

So, how does it affect the rich and super rich who would have share portfolios over $728,000 and probably in the millions?

Average dividend yield is 4.1%

Re: Abbott/Liberal Govt Watch

![]() by Q. » Sun Mar 03, 2019 8:16 pm

by Q. » Sun Mar 03, 2019 8:16 pm

Jimmy_041 wrote:Q. wrote:

Most of the other 50% are retirees who pay no tax. I'm suggesting that if you remove the excess credit for everyone, then you remove a government handout for high income earners who clearly don't need a government handout.Have you got a source for that statement?

You aren't seriously stating that most of the people earning less than $180kpa don't have dividend paying shares

Do the math. 92 per cent of taxpayers do not claim excess franking credits through their personal income tax return. The median wage in Aus is $55,000. They don't earn enough to get a franking credit refund. So common sense, says that most of the other 50% is made up a non-taxpaying retirees.

Yes, that is what I'm saying. People with a net wealth decile from $0 to $944,,000 hold a total of 7.4% of the value of all shares held.

Re: Abbott/Liberal Govt Watch

![]() by Q. » Sun Mar 03, 2019 8:23 pm

by Q. » Sun Mar 03, 2019 8:23 pm

Jimmy_041 wrote:DOC wrote:Couples, income split. One has the relevant shares in their name and have an income below the tax threshold.

Quote Jim "It doesn't affect investors with a portfolio providing annual dividends higher than $37,000 who are in a higher tax bracket than the company tax."

They still have the first bit tax free, the next at 19c so the overall rate is lower.

Income of $40 k is not all at 30c, but 18K zero and the next 19K 19c then the last 3K at 32.5c, which would give a tax rate of about 9.5c.

Correct, but you can only do that if you invested through a trust. We didn't have one in the 90's so most of our shares are in my wife's name to minimise the tax, but, the main point is: as you earn more; you pay tax and therefore you reap the benefit of the excess credits.

So; it actually targets the lower and middle class, and in all probably, never the wealthy.

This is what Robert Gottliebsen is saying.

I might add; it applied to pensioners as well until they did a massive backflip and added the Pensioner Guarantee

https://www.theguardian.com/australia-news/2018/mar/27/labor-offers-pensioner-guarantee-as-tax-policy-divides-voters-guardian-essential-poll

You're being disingenuous. Big difference between taxable income and actual income - given that a pension from superannuation is tax-free.

Taxable incomes from $0 to $9500 claim 30% of excess franking credits - ie. people who draw a tax free pension from super.

Re: Abbott/Liberal Govt Watch

![]() by DOC » Sun Mar 03, 2019 9:35 pm

by DOC » Sun Mar 03, 2019 9:35 pm

Not all. Many government schemes do not qualify where there is a defined benefit or the amount of pension is over $100K.

One of the very few things that GOVT workers are behind on.

One of the very few things that GOVT workers are behind on.

Re: Abbott/Liberal Govt Watch

![]() by Jimmy_041 » Sun Mar 03, 2019 9:38 pm

by Jimmy_041 » Sun Mar 03, 2019 9:38 pm

Q. wrote:Jimmy_041 wrote:DOC wrote:Couples, income split. One has the relevant shares in their name and have an income below the tax threshold.

Quote Jim "It doesn't affect investors with a portfolio providing annual dividends higher than $37,000 who are in a higher tax bracket than the company tax."

They still have the first bit tax free, the next at 19c so the overall rate is lower.

Income of $40 k is not all at 30c, but 18K zero and the next 19K 19c then the last 3K at 32.5c, which would give a tax rate of about 9.5c.

Correct, but you can only do that if you invested through a trust. We didn't have one in the 90's so most of our shares are in my wife's name to minimise the tax, but, the main point is: as you earn more; you pay tax and therefore you reap the benefit of the excess credits.

So; it actually targets the lower and middle class, and in all probably, never the wealthy.

This is what Robert Gottliebsen is saying.

I might add; it applied to pensioners as well until they did a massive backflip and added the Pensioner Guarantee

https://www.theguardian.com/australia-news/2018/mar/27/labor-offers-pensioner-guarantee-as-tax-policy-divides-voters-guardian-essential-poll

You're being disingenuous. Big difference between taxable income and actual income - given that a pension from superannuation is tax-free.

Taxable incomes from $0 to $9500 claim 30% of excess franking credits - ie. people who draw a tax free pension from super.

I'm not being disingenuous at all. I said lets put super aside and look at these so called "rich" people with assets outside super who this policy is meant to target. We have already established that you can have $1.4m super inside an industry fund (or be a government employee) and wont be touched yet those with half that in a SMSF will be affected.

So I am now looking at people with investments outside super. I am trying to find these so called "wealthy" people who are being targeted by this Labor plan. My example shows that the wealthy wont be touched because they will still have taxable income whereas those retirees with a low dividend income lose. Am I wrong?

dedja: Dunno, I’m just an idiot.

Re: Abbott/Liberal Govt Watch

![]() by Jimmy_041 » Sun Mar 03, 2019 10:12 pm

by Jimmy_041 » Sun Mar 03, 2019 10:12 pm

Q. wrote:Jimmy_041 wrote:Q. wrote:

Most of the other 50% are retirees who pay no tax. I'm suggesting that if you remove the excess credit for everyone, then you remove a government handout for high income earners who clearly don't need a government handout.

You aren't seriously stating that most of the people earning less than $180kpa don't have dividend paying shares

Do the math. 92 per cent of taxpayers do not claim excess franking credits through their personal income tax return. The median wage in Aus is $55,000. They don't earn enough to get a franking credit refund. So common sense, says that most of the other 50% is made up a non-taxpaying retirees.

Yes, that is what I'm saying. People with a net wealth decile from $0 to $944,,000 hold a total of 7.4% of the value of all shares held.

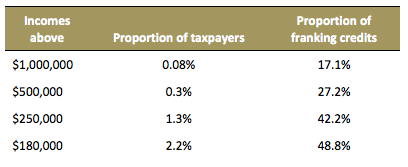

Huh? No, I don't accept your math. According to this chart you posted, 97.8% of taxpayers earn less than $180k and get 51.2% of franking credits (which I assume are all franking credits). To say the majority of these franking credits are going to retirees who pay no tax is ludicrous

Common sense? Common sense says absolute bollocks! Show me the data, report or credible source to back up your statement.

dedja: Dunno, I’m just an idiot.

Re: Abbott/Liberal Govt Watch

![]() by Jimmy_041 » Mon Mar 04, 2019 8:49 am

by Jimmy_041 » Mon Mar 04, 2019 8:49 am

From the AFR this morning

This is exactly my point. The wealthy will not be hit. It’s the low to middle who will bear the brunt. The fact that Labor had to do a massive backflip and bring in the “Pensioner Guarantee” means either:

1. They meant to include all pensioners

2. They have NFI how their policy works

The fact that they say it targets the wealthy means:

1. They are effing lying

2. They have NFI how their policy works

Wealthier shareholders will be less affected because they tend to have tax liabilities and can therefore fully use imputation credits. People with more than $1.6 million in superannuation will have moved any excess into their accumulation account, where it is taxed at 15 per cent. They will be able to use their tax credits to offset this liability. But for those who pay no tax, the credits will go to waste.

This is exactly my point. The wealthy will not be hit. It’s the low to middle who will bear the brunt. The fact that Labor had to do a massive backflip and bring in the “Pensioner Guarantee” means either:

1. They meant to include all pensioners

2. They have NFI how their policy works

The fact that they say it targets the wealthy means:

1. They are effing lying

2. They have NFI how their policy works

dedja: Dunno, I’m just an idiot.

Re: Abbott/Liberal Govt Watch

![]() by Q. » Mon Mar 04, 2019 8:50 am

by Q. » Mon Mar 04, 2019 8:50 am

Jimmy_041 wrote:Q. wrote:Jimmy_041 wrote:Q. wrote:

Most of the other 50% are retirees who pay no tax. I'm suggesting that if you remove the excess credit for everyone, then you remove a government handout for high income earners who clearly don't need a government handout.

You aren't seriously stating that most of the people earning less than $180kpa don't have dividend paying shares

Do the math. 92 per cent of taxpayers do not claim excess franking credits through their personal income tax return. The median wage in Aus is $55,000. They don't earn enough to get a franking credit refund. So common sense, says that most of the other 50% is made up a non-taxpaying retirees.

Yes, that is what I'm saying. People with a net wealth decile from $0 to $944,,000 hold a total of 7.4% of the value of all shares held.

Huh? No, I don't accept your math. According to this chart you posted, 97.8% of taxpayers earn less than $180k and get 51.2% of franking credits (which I assume are all franking credits). To say the majority of these franking credits are going to retirees who pay no tax is ludicrous

Common sense? Common sense says absolute bollocks! Show me the data, report or credible source to back up your statement.

I've posted the stats above. Let's go over it again.

92% of the population does not claim excess franking credits. Non-pensioner recipients of refunds of franking credits constitute just 4

percent of the adult population. Which leaves the other 4% being mostly retired non-pensioners aged 65 and over with no tax liability - of which 85% are in the top wealth quintile of households.

As I stated above, people in the three highest wealth deciles ($944K and above) hold 92.6% of all shares in Australia.

This policy does not affect low and middle income earners. Stop saying it does.

Re: Abbott/Liberal Govt Watch

![]() by Q. » Mon Mar 04, 2019 8:51 am

by Q. » Mon Mar 04, 2019 8:51 am

And all this data is freely available from the PBO papers.

Re: Abbott/Liberal Govt Watch

![]() by Jimmy_041 » Mon Mar 04, 2019 12:08 pm

by Jimmy_041 » Mon Mar 04, 2019 12:08 pm

Q. wrote: I've posted the stats above. Let's go over it again.

92% of the population does not claim excess franking credits. Non-pensioner recipients of refunds of franking credits constitute just 4

percent of the adult population. Which leaves the other 4% being mostly retired non-pensioners aged 65 and over with no tax liability - of which 85% are in the top wealth quintile of households.

As I stated above, people in the three highest wealth deciles ($944K and above) hold 92.6% of all shares in Australia.

This policy does not affect low and middle income earners. Stop saying it does.

You had better tell that to the avalanche of people saying it does. I'm prepared to listen to them because it makes sense if you (are prepared to) understand the tax system.

Seeing you cant argue with my examples of how this will actually affect lower - middle income earners instead of the wealthy (which Labor claim will be the main losers) I will post again what was written in the AFR. Some more people you know better than:

Wake-up call for investors facing lower returns in Labor franking plan

William McInnes

Mar 1, 2019 — 11.00pm

Some investors will need a serious reshuffle of their investment portfolios to avoid losing regular income if Labor wins the election and scraps the refund of excess franking credits.

While some wealth advisers say the proposed changes could be positive in that they will mean more diversified portfolios, they add the changes could also mean investors look to asset classes they don't understand in search of regular income.

"Investors shouldn't be reactive to this and they shouldn't suddenly start looking at investments they don't understand because without advice they can make big mistakes," says Sentinel Wealth managing director Justin Hooper. "The fact that dividend yields have historically been higher in Australia means investors have got used to this situation and now they're being reactive."

The Australian equity market returns far more to shareholders through dividend distribution than other global markets and the complacency of local investors has meant they are often unaware of other investment options. Simon Letch

The current earnings season has shown that the appetite for companies to pay out dividends to shareholders is still well and truly alive, with the amount of dividends paid set to hit a record high of $84 billion in 2018-19.

Providence Wealth managing director Grant Patterson is worried investors who will receive less income under the Labor proposal will try to chase higher returns through assets they don't fully understand. "Our concern would be if the rules change and investors are trying to replace that income, it may result in chasing income that would increase the risk in their portfolio," he says.

Under Australia's system of dividend imputation, shareholders receive franking credits to account for tax paid at the corporate level, which in most cases is 30 per cent. Credits can be used to offset tax owed by the shareholder.For people who pay little or no tax (such as superannuation funds and retirees), excess franking credits are paid out as cash refunds. Labor will end those refunds, except for people covered by its "pensioner guarantee". The guarantee means anybody receiving a Centrelink age pension will still be eligible for refunds. A limited exclusion for SMSFs applies only if one member was receiving a part or full pension before March 28, 2018.

Wealthier shareholders will be less affected because they tend to have tax liabilities and can therefore fully use imputation credits. People with more than $1.6 million in superannuation will have moved any excess into their accumulation account, where it is taxed at 15 per cent. They will be able to use their tax credits to offset this liability. But for those who pay no tax, the credits will go to waste.

While investors with larger balances (paying tax) won't be hit, Hamilton Wealth Management managing partner Will Hamilton says the changes will leave investors with smaller balances (paying no tax) in the lurch. As the table shows, those paying higher levels of tax won't be worse off under the proposed change but those on zero or 15 per cent tax will be worse off because they will no longer receive a tax refund.

"We've had new clients that have come to see us and it's a big discussion," Hamilton says. "The sophisticated investor can prepare for this. Some people have a lot of money and have still struggled with this conversation. It's the impact on smaller balances where I do feel the shadow treasurer doesn't quite realise what he's done."

Mason Stevens portfolio manager Alwyn Hung says those with taxable income are better protected from the proposed changes while lower-rate taxpayers would be hit hardest.

"The community of net losers if the Labor party were to win office and implement this change would be, for the most part, those that have tax liabilities less than the value of the franking credits. Broadly speaking, these are not-for-profit organisations, self-funded retirees, self-managed super funds (SMSFs) and income earners earning less than $18,200 and exempt from tax."

The Australian equity market returns far more to shareholders through dividend distribution than other global markets and the complacency of local investors has meant they are often unaware of other investment options.

"The one positive will be that there will be some discipline towards asset allocation," Hamilton says. "I don't agree with people having 100 per cent cash and Australian equities.

Investors should consider alternatives with caution, says Sentinel Wealth's Justin Hooper. Daniel Munoz

"There's a familiarity that sometimes does breed contempt. They're using the system and supplementing their income by investing long in Australia equities. [But] people have made plans based on the laws that have existed and these people do things themselves. If they look to diversify, there's going to be another cost from that."

Hamilton says many smaller investors have expressed concerns about trying to readjust their portfolios, particularly those unable to pay for professional advice.

"They're really worried. Suddenly that tap [of refunded franking credits] is going to be turned off and it's really sad. They can't go and [reallocate assets] to the same extent."

Despite concerns the changes will force investors away from assets they know and understand, advisers believe there could be some unintended positive consequences.

Providence Wealth's Grant Patterson is worried investors who will receive less income under the Labor proposal will try to chase higher returns through assets they don't fully understand. Peter Braig

Where to invest instead

The implementation of Labor's franking policy would be just the latest hurdle for dividend-chasing investors. The blue-chip dividend stars of yesteryear have disappointed in the last few months and while the big iron ore miners have paid generous dividends in the past few months, they are heavily exposed to the fluctuations of the commodity cycle.

"What people have to do is change the focus. Stop looking at the yield and start looking at the total returns," Hamilton says. "Look at growth companies, international equities or, if their risk appetite is correct, some alternate debts products."

Sentinel Wealth financial planner Jon James believes investors need to have a strong objective and find the right portfolio to match that objective.

"It really does come back to your asset allocation and having a strategy," he says. "One of the concerns we have is people abandoning their investment strategy because they'll introduce some additional risk into their portfolio."

Bond proxies

Advisors say bond proxy stocks, such as infrastructure and real estate investment trusts (REITs), are a good option for investors looking for regular income and are already well understood by equity investors.

REITS and infrastructure stocks are closely linked to the bond market due to their high levels of debts, with investment spurred by lower interest rates.

They can offer predictable returns, with revenue streams similar to bonds. Due to the defensive nature of infrastructure stocks, they can typically offer a greater level of certainty for investors than other sectors.

"Some of the infrastructure stocks on the ASX and the real estate investment trusts are certainly options clients might look at," Sentinel Wealth's James says.

Providence's Patterson says both sectors are likely to provide good income. "[Infrastructure] has its own dynamics but it traditionally pays a reasonable income because it's very highly geared. The real estate investment trust sector might also attract more interest because of the distribution yield."

According to data from Factset, the dividend yield of the S&P/ASX 200 is about 4.6 per cent and 6.1 per cent after franking, making it relatively attractive compared with real estate investment trusts at 5.5 per cent with no franking and utility stocks at 5.1 per cent with no franking.

Were franking credits to be removed, stocks like Transurban, Sydney Airport, Spark Infrastructure and Atlas Arteria would look significantly more attractive from an income perspective relative to the S&P/ASX 200.

Corporate bonds

Corporate bonds could also provide a reasonable level of income to investors, although advisers are cautious on the risks surrounding them.

"People might look at corporate debt instruments," says Sentinel's James. "However when people move into the corporate bond world, the overall risk is a concern."

Corporate regulator the Australian Securities and Investments Commission says it is vital investors know the risks associated with corporate bonds.

"The main risk with corporate bonds is that you may not receive interest payments or get your money back if the company issuing the bonds goes out of business," it highlights.

ASIC recommends assessing the business environment the company operates in, including looking which country it is in, what the outlook for the industry is and the strength of management.

Providence's Patterson agrees, saying that while debt markets can diversify a portfolio, investors need to be aware of the elevated risks.

"The potential positive in returning the franking is Australian shares become less attractive at the margin and portfolios might become more diversified," he says. "It may mean investors focus more on corporate bonds but they need to understand the risk of credit markets. As we saw in the global financial crisis, credit markets basically imploded."

Income trusts

Hybrid securities are another asset class often used by not-for-profit organisations, SMSFs and self-funded retirees as a proxy for fixed income, with the added benefits of franking.

Hybrids are also set to be impacted under franking changes, with the dividends being paid out from them subject to the same rules as equity investments. Mason Stevens' Hung says: "The proposed tax changes may mean they need to rethink this strategy."

A note from Bell Potter analysts Damien Williamson and Barry Ziegler in early February suggested investors in hybrid securities could shift some of their investments to an income trust to avoid losing their tax refund.

"In quantifying the impact on an SMSF with a $600,000 investment in Westpac Capital Notes 5 generating $22,050 cash and $9,450 in franking credits, the SMSF would lose a surplus franking cash rebate of $4,725 under the ALP policy," they said. "To maintain the same level of after-tax income, this investor may reallocate half their Westpac Capital Notes 5 holding into an investment such as NB Global Corporate Income Trust."

They added the move by investors away from the capital structure of banks to offshore investments would likely increase bank funding costs and limit government revenue. "This investment strategy also brings into question the quantum of revenue this policy will generate," the Bell Potter analysts add.

Overseas shares

Buying overseas shares, where the total returns and prospect of share buybacks are greater, could also be another option for investors searching for income.

Hamilton says overseas markets are becoming better understood by investors. "If you spoke to people 15 years ago about international equities, they weren't as popular."

Most advisors agree that international equities should form a part of any diversified portfolio but say the income stream isn't as simple.

"[International equities] have got to be part of your overall investment strategy," says Sentinel's James. "You shouldn't just be going overseas to search for dividend yield. So by going to the US market, you're not necessarily going to get a very high yield but they generally have higher capital growth. You're also exposed to currency movements."

Providence's Grant is more sceptical. "Investors are unlikely to go to international equities because it won't provide enough income," he says. "Overseas companies' excess capital is used to buy back shares rather than dividends. I don't see it as a replacement for people requiring income."

Additional reporting by Joanna Mather.

Last post. I've got work to do and you aren't prepared to accept any alternative argument anyway.

I guess that's what happens when people only read what they know will support their already set views.

dedja: Dunno, I’m just an idiot.

Re: Abbott/Liberal Govt Watch

![]() by Q. » Mon Mar 04, 2019 12:24 pm

by Q. » Mon Mar 04, 2019 12:24 pm

Jimmy_041 wrote:Last post. I've got work to do and you aren't prepared to accept any alternative argument anyway.

I guess that's what happens when people only read what they know will support their already set views.

You seem averse to the statistics and keep quoting articles that use above average superannuation portfolios as examples (and tag them as 'middle income').

Average superannuation balances at the time of retirement (assumed to be age 60 to 64) in 2015-16 were $270,710 for men and $157,050 for women.

This policy doesn't affect low and middle income earners.

Re: Abbott/Liberal Govt Watch

![]() by Jimmy_041 » Mon Mar 04, 2019 12:36 pm

by Jimmy_041 » Mon Mar 04, 2019 12:36 pm

Q. wrote:Jimmy_041 wrote:Last post. I've got work to do and you aren't prepared to accept any alternative argument anyway.

I guess that's what happens when people only read what they know will support their already set views.

You seem averse to the statistics and keep quoting articles that use above average superannuation portfolios as examples (and tag them as 'middle income').

Average superannuation balances at the time of retirement (assumed to be age 60 to 64) in 2015-16 were $270,710 for men and $157,050 for women.

This policy doesn't affect low and middle income earners.

No; I’m adverse to you quoting statistics that have nothing to do with what I am saying. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. Your average super balance supports what I am saying. If everyone had $2m they could get around it and that’s what the wealthy will do

I don’t think you actually read what I post or quote.

Plus the Labor policy is based upon current investment traits. People will adapt and Labors projections will be way out. You can read that in most of the articles I posted.

dedja: Dunno, I’m just an idiot.

Re: Abbott/Liberal Govt Watch

![]() by Q. » Mon Mar 04, 2019 12:47 pm

by Q. » Mon Mar 04, 2019 12:47 pm

Jimmy_041 wrote:Q. wrote:Jimmy_041 wrote:Last post. I've got work to do and you aren't prepared to accept any alternative argument anyway.

I guess that's what happens when people only read what they know will support their already set views.

You seem averse to the statistics and keep quoting articles that use above average superannuation portfolios as examples (and tag them as 'middle income').

Average superannuation balances at the time of retirement (assumed to be age 60 to 64) in 2015-16 were $270,710 for men and $157,050 for women.

This policy doesn't affect low and middle income earners.

No; I’m adverse to you quoting statistics that have nothing to do with what I am saying. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. Your average super balance supports what I am saying. If everyone had $2m they could get around it and that’s what the wealthy will do

I don’t think you actually read what I post or quote.

Plus the Labor policy is based upon current investment traits. People will adapt and Labors projections will be way out. You can read that in most of the articles I posted.

Low and middle class don't claim excess franking credits! As I wrote above:

92% of the population does not claim excess franking credits. Non-pensioner recipients of refunds of franking credits constitute just 4

percent of the adult population. Which leaves the other 4% being mostly retired non-pensioners aged 65 and over with no tax liability - of which 85% are in the top wealth quintile of households.

Re: Abbott/Liberal Govt Watch

![]() by Q. » Mon Mar 04, 2019 12:50 pm

by Q. » Mon Mar 04, 2019 12:50 pm

I do agree with you that many portfolios will be shuffled around, in particular moving to accumulation phase and I don't think we will see a true saving of $8bil.

As I wrote earlier, move to a model that most of the OECD uses, whereby those claiming a franking credit refund can only claim a part % (ie. up to 25%), while also abolishing the tax-free franking credit refund.

As I wrote earlier, move to a model that most of the OECD uses, whereby those claiming a franking credit refund can only claim a part % (ie. up to 25%), while also abolishing the tax-free franking credit refund.

Last edited by Q. on Mon Mar 04, 2019 12:51 pm, edited 1 time in total.

Re: Abbott/Liberal Govt Watch

![]() by Jimmy_041 » Mon Mar 04, 2019 12:51 pm

by Jimmy_041 » Mon Mar 04, 2019 12:51 pm

**** me!

The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t.

The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t.

dedja: Dunno, I’m just an idiot.

Re: Abbott/Liberal Govt Watch

![]() by Q. » Mon Mar 04, 2019 12:54 pm

by Q. » Mon Mar 04, 2019 12:54 pm

Jimmy_041 wrote:**** me!

The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t.

Lower and middle class don't claim franking credit refunds therefore are unaffacted.

Re: Abbott/Liberal Govt Watch

![]() by Jimmy_041 » Mon Mar 04, 2019 1:14 pm

by Jimmy_041 » Mon Mar 04, 2019 1:14 pm

Q. wrote:Jimmy_041 wrote:**** me!

The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t. The wealthy have the means to get around this policy via Super and direct investments. The lower classes don’t.

Lower and middle class don't claim franking credit refunds therefore are unaffacted.

Yeah I give up

](./images/smilies/eusa_wall.gif "Brick wall")

dedja: Dunno, I’m just an idiot.

Board index

Who is online

Users browsing this forum: No registered users and 53 guests